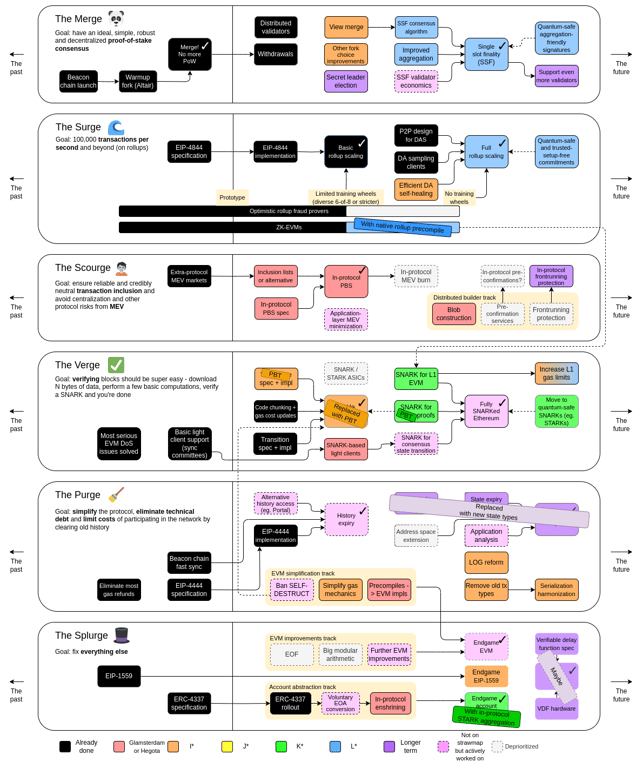

I updated my 2023 roadmap diagram to overlay where the items that were there sit in the current Strawmap ( https://strawmap.org/ ).

In general, a lot of overlap, but:

* Some things got reshuffled in order (eg. quantum safety up-prioritized)

* Some things deprioritized (eg. VDFs; many EVM improvements)

* Some things replaced with superior constructions (eg. Verkle -> unified BT -> PBT; state expiry -> new state types)

What's most striking, however, is that some completely new things are in the strawmap that are NOT in this diagram, because they were not in the 2023 roadmap at all. These reflect changing priorities.

Notably:

* First-class attention to strong privacy. This covers: keyed nonces and recent roots, aspects of FOCIL, lean privacy pool & wormholes

* Aggressive scaling in the context of post-quantum. This covers: leanSPHINCS signatures and aggregation, zkzk frames (see https://ethereum-magicians.org/t/eip-828… )

* Lean-ification of the spec, to assist in formal verification (full FV of everything is only possible because of modern AI)

* Blob and gas futures (this idea just didn't exist back in 2023)

* Native rollups (SNARKs were nowhere near mature enough to even consider this back in 2023)

* A more open design space for the "future of the EVM". zkzk frames already implies that the protocol will expose to users some ISA that's not the EVM - current leading candidates are leanISA and RISC-V. These ISAs are more simple, modern and efficient than the EVM. Once they're there, why not expose them to developers everywhere? (And then, why not turn the EVM into being an IR on top of that ISA, instead of an enshrined feature massively complicating the base protocol?) Though much of the deeper exploration here is too early even for the strawmap.

* New state types are not just a replacement for expiry, they're a fundamentally different paradigm to how Ethereum does scaling

A common theme in scaling, found in both state types and zkzk frames (both new ideas), is that instead of trying to maximally scale ALL ethereum activity, we try to create specialized mechanisms that have more restrictive properties that make them more scaling-friendly, while supporting the heaviest loads incurred by users and applications today (eg. token transfers, swaps) and tomorrow (eg. privacy protocols).

The other common theme is treating STARKs and AI-accelerated FV as first-class objects, that we are okay betting the technical future of Ethereum on. There are recursive STARKs in many layers of the protocol, one particular primitive (the "aggregate to union verified dependencies" primitive) is expected to be used in *three* places in the protocol: EL, CL and DL. This can only be safe with formal verification, which is itself only feasible with modern AI tools.

In general, many steps forward in maturity. And a huge amount of hard work by many dozens of Ethereum researchers and developers on all of these features.

Ethereum will be quantum-safe. Ethereum will put users' privacy first. Ethereum will be secure. Ethereum will be censorship-resistant. Ethereum will be highly performant and scalable while satisfying the above. And Ethereum will be Lean.